Thanks to the economic downturn and a surge in the nation’s transient population, renters now outnumber homeowners in six of the 10 most populous cities in the US. However, many renters aren’t taking proper precautions against the risks inherent in their style of living.

According to the Bureau of Justice Statistics, renters are 50% more likely to experience theft than those who own their own homes—yet 67% of the nation’s renters don’t carry renters insurance.

An Apartments.com survey of renters reveals the excuse for the exclusion is a simple one: affordability.

While most producers who offer renters insurance argue that that the premium is relatively inexpensive, it’s hard to convince a Manhattan resident to add to their average rental bill of $3,350 a month.

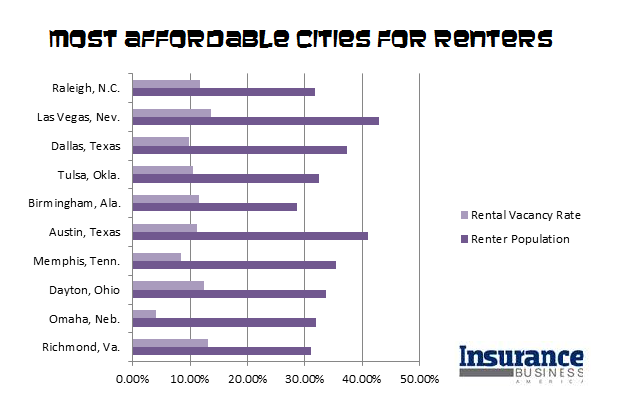

Renters in these 10 cities are a better bet. Based on average monthly salaries and the average price of rent, folks here are getting a comparatively good deal on their living expenses, making them more likely to spring for an insurance policy.

At least a third of residents each city here are renting property, with plenty of room to grow in vacant units. And with rent prices at roughly a third of average monthly income, an annual renters insurance premium of $200 a month isn’t a big ask.

Even in cities like San Francisco, where rent is far above the nationwide average of $899, skilled producers can make a renters policy an attractive and palatable option through carrier discounts.

“If you sign a client up for renters and auto insurance with the same company, usually there’s a 15% discount on both policies,” said Jerry Becerra, president of Barbary Insurance Brokerage. “That makes a big difference. Really, renters insurance practically pays for itself.”

Becerra has already been experiencing a surge of renters purchases at his agency, as millenials come of age and more Americans choose the flexibility of a rental unit. With the surge comes more than one type of insurance sale.

“I’ve also been selling a number of liability policies. People are really worried about their liability, particularly older people,” he said. “If you overflow the bathtub and it ruins the unit below you, you have some personal liability for that. Having coverage makes a big difference.”

Getting consumers to that point, however, is difficult.

“I think people are afraid of the cost and don’t realize it’s very inexpensive and sometimes even a savings,” Becerra said. “Other people aren’t even aware it’s available. I don’t see that many people saying, ‘Oh, I need a renters policy.’”

Once Becerra manages to close the deal, however, he manages to retain a high number of clients—both for renters insurance and other policies.

“Once people buy coverage and realize it’s not a big expense, they usually maintain it,” he said.

Producers who manage to break into this market are likely to enjoy returns for some time, said Ann Myhr, a senior director of knowledge resources with

The Institutes.

“Indicators are that renting is going to continue to be on the upswing for the foreseeable future,” she said. “I think you’ll continue to see that, particularly in certain areas of the country, younger folks at this point in time don’t have a big interest in owning a home.”

You may also enjoy: "The vital renters insurance policy change you're not making"

"Domestic Violence Awareness Month: How producers can help victims find freedom"

"The top 5 states for auto, homeowners hikes in 2013"