Young, healthy Americans are seeing the highest increases in their health insurance premiums following the conclusion of the Affordable Care Act’s second open enrollment period.

According to a recent analysis from The Heritage Foundation, non-group health insurance premiums increased on average 5.3% from 2014 to 2015—relatively in line with what analysts expected. For the nation’s 27-year-olds, however, premiums shot up 8.46%.

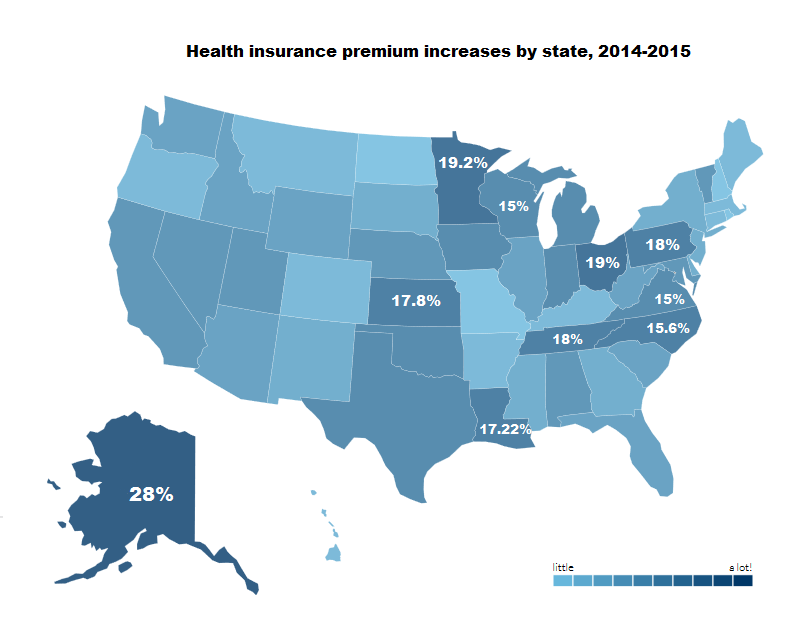

Averages don’t tell the whole story, however. There was significant variation in premiums within the same tier even at the state level, and young Americans in some states found their premium costs increasing at a slower clip, or even decreasing in some cases.

New Hampshire residents saw the most favorable changes in its rates, with health insurance premiums falling 4% for the average 27-year-old. Young people in Missouri (-2%), Rhode Island (-1.36%) and North Dakota (-1%) also so modest decreases in their insurance bills.

On the opposite end of the spectrum, young ACA enrollees in Alaska saw their premiums shoot up a whopping 28% from $216.12 per month in 2014 to $235.57 in 2015. This is in line with the 28% increase among 50-year-old Alaskans as well as the 24% increase for family rates.

Alaska has long been among the most expensive health insurance markets in the country, a problem lying with the state’s unique geography and lack of local providers.

“Alaska’s healthcare market [is] dominated by small, rural and independent providers,” says AK Health Reform, a coalition of Alaskan healthcare associations. “Alaska lacks a centralized knowledge repository and unified communication channel.”

Other states with high premium spikes for young people include: Minnesota (19.2%), Ohio (19%), Pennsylvania (18%), Tennessee (18%), Kansas (17.8%), Louisiana (17.22%), North Carolina (15.6%) and Virginia (15%).

In general, health insurance carriers have had to make up for lost ground after setting rates that were too optimistic—perhaps a consequence of the ACA’s directive that insurance actuaries use age slopes of 3:1, as opposed to the 5:1, 6:1 or 7:1 slopes insurers generally employ.

Stanley Sieniawski, president of InsureOne Benefits in Litchfield, Ohio, also believes allowing individuals to stay on their parents’ health insurance plans until the age of 26 has had “unintended consequences” on health insurance affordability for young people.

“The majority of individuals under the age of 26 are staying out of the individual market, and they’re the very people carriers want to offset the risk of older people buying coverage,” said Sieniawski, who works solely with the individual market in his practices.

“You’ve got a perfect storm whereby the insurance companies are not attracting risk either because they’re staying on mom and dad’s policy, they don’t believe the need insurance or even with subsidies, they are not able to afford it because of these rate increases.”

Despite the sometimes shocking increases, researchers with the Heritage Foundation say the premium spikes are not wholly unexpected in a market experiencing disruptive changes.

“The real-world effect for most exchange consumers is that the prices they pay further increased in 2015, though not as dramatically as they did in 2014,” The Heritage Foundation.

You may also be interested in: "The most expensive health insurance markets of 2015: Kaiser"

"Just how high has the ACA pushed premiums?"

"Obamacare exchanges to offer just one plan for many small employer"